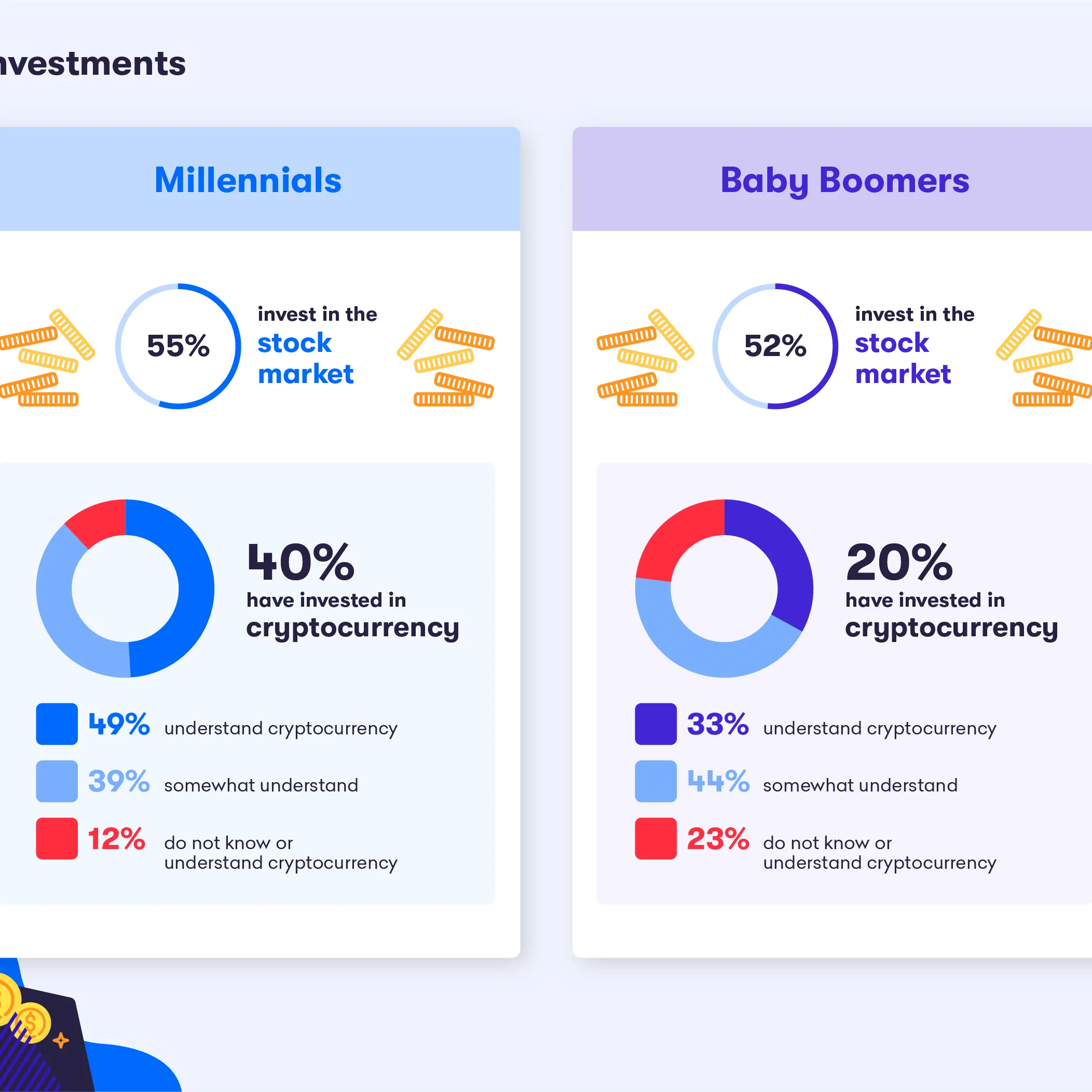

A recent study has revealed that the average Baby Boomer has nearly double the amount of savings compared to Millennials, highlighting a significant generational financial gap. According to the data, Baby Boomers, who are typically defined as those born between 1946 and 1964, hold an average of $170,000 in savings. In contrast, Millennials—those born between 1981 and 1996—have been able to accumulate an average of only $90,000 in savings.

Experts attribute this disparity to several factors, including differences in income levels, economic circumstances at the time of entering the workforce, and varying spending habits. As Baby Boomers began their careers in an era of rising wages and relative economic certainty, they capitalized on robust job markets, paving the way for higher savings. Conversely, Millennials have faced tougher economic conditions, including the aftermath of the 2008 financial crisis and the ongoing impacts of the COVID-19 pandemic, which severely affected job prospects and earning potential.

“These generational differences in savings are stark and concerning,” said Barbara Smith, a financial planner based in New York. “Millennials are often stuck dealing with high student loan debts and the rising costs of living, which hinder their ability to save at a similar rate to their predecessors.”

The findings underscore a need for Millennials to reassess their financial strategies in order to bridge the growing savings gap as they plan for future financial stability. Policy experts suggest that structural changes, such as improving access to affordable housing and student debt relief, could help Millennials increase their savings.