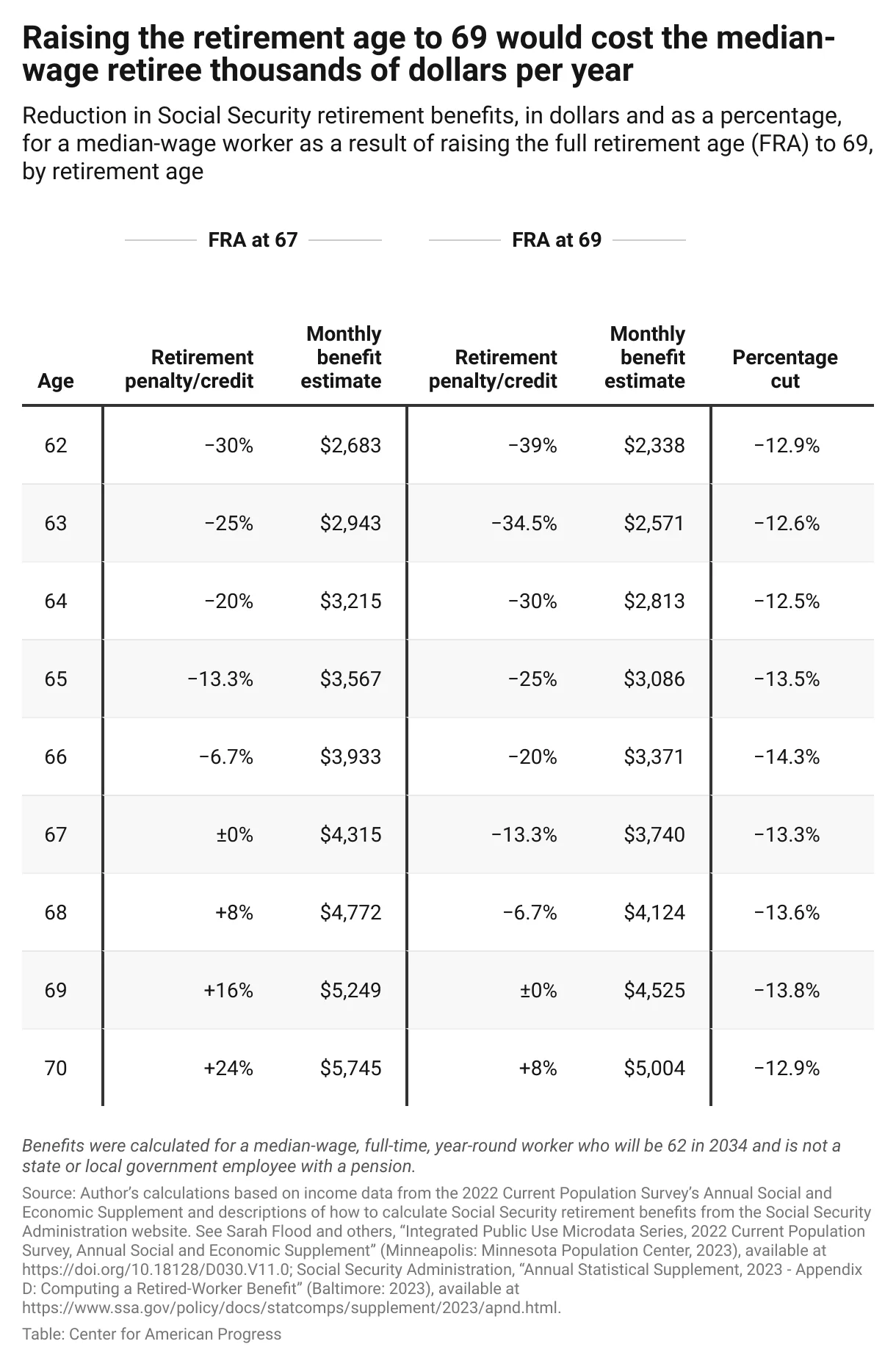

As 2025 approaches, retirees and future beneficiaries of Social Security are set to experience significant changes. One of the most notable adjustments is the increase in the retirement age for full benefits to 67 years for those born in 1960 or later. Historically, the full retirement age has been gradually rising since the 1980s when it was adjusted from 65 to 67 for future retirees. This change aims to address funding shortfalls in the Social Security program, which are exacerbated by the increasing life expectancy of Americans.

Additionally, the Social Security Administration (SSA) has announced a substantial increase in monthly benefits due to the Cost-of-Living Adjustment (COLA), which is expected to rise by 3.2% in 2025, reflecting inflationary pressures and higher living costs. This adjustment touches on the maximum monthly benefit available, which is projected to reach $4,028 for those who retire at their full retirement age.

Furthermore, the Social Security Trust Fund, which is responsible for paying out benefits, is anticipated to begin depleting its reserves by 2035, potentially leading to reduced benefits unless legislative reforms are implemented. Currently, if no action is taken, beneficiaries may only receive about 80% of their scheduled benefits in the future.

Financial planners stress the importance of understanding these changes. “It’s vital for individuals nearing retirement to modify their planning strategies according to these upcoming adjustments to ensure a secure financial future,” advised financial advisor Martin Bell. The COLA increase is particularly crucial for low-income retirees who depend heavily on Social Security as their primary source of income.

As these changes unfold, it’s increasingly important for beneficiaries to stay informed and proactive in managing their retirement plans.